The evidence is everywhere, yet only visible to some. We are in the midst of a historical battle over the future shape of money. To give a sense of the shift, a recent discussion paper from the Bank of England illustrates a scenario in which 20% of deposits will siphon off from commercial bank accounts to “new digital money”, meaning FinTech applications, cryptocurrencies and stablecoins, as well as new central bank-issued digital currencies.

In this emerging landscape, questions – about the disappearance of cash, of who gets to ‘print’ new digital moneys or trillion-dollar coins and control their circulation, and even decide de facto monetary policies – are all being renegotiated between central banks, governments, technology companies and commercial banks. Meanwhile, crypto-enthusiasts, excited about the uses of their favourite tech, are disrupting, prodding or playing along, to the alternating excitement and dismay of community currency activists. It is not yet clear who has our interests best at heart.

Let me briefly present three exhibits that offer glimpses of a landscape that is radically shifting.

Exhibit A: Tokenization

Money is rapidly changing form, from physical cash to digital payment systems. Writer Brett Scott points out that this is the privatisation of payments, entailing a shift in power to private banks.

But digital money also has its dissidents, artists and con-artists. Earlier attempts at creating digital cash, in Bitcoin and other projects, have instead spurred a wave of experimentation in other types of digital expressions of value – arguably no longer money at all – but a variety of tokens.

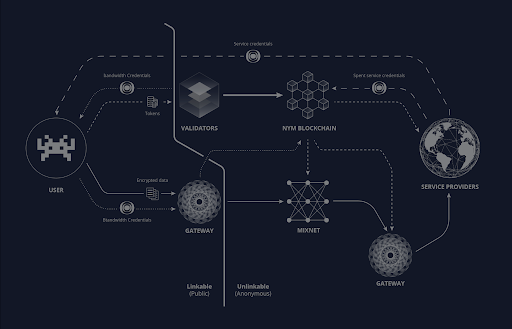

It is worth looking at an example. I recently started working for a technology company called Nym. The aim is to establish a decentralised network that provides privacy for internet traffic. Nym includes a token rewarding people who run the nodes in the network.

For an ordinary person wanting to use this system, tokens work like chips at a funfair. You buy these with ‘normal’ money, which can then be spent on rides. The ‘funfair’, in this example, is a privacy network and the ‘rides’ are different privacy-preserving digital services.

But tokens don’t just grant access. They can serve a variety of other purposes internally in the network: measuring the reputations of different nodes; rewarding them for their work; assigning ‘voting power’; signalling demand and capacity; carrying out accounting; securing against specific attacks; and more – with the overall supply and distribution of tokens partially ‘regulated’ through algorithms.

This is all characteristic of an emerging and controversial field of ‘cryptoeconomics’, governing the internal dynamics of decentralised networks. In other words, the ‘funfair’ might equally be an energy grid or a social network; and they might include ‘payment tokens’, ‘utility tokens’, and more.

Sometimes described as ‘moving castles’, these decentralised networks are being engineered as discrete digital realms, with tokens organising internal resources, developers busy building and LARPing new communities into existence.

But it is not at all easy to see where these cryptoeconomic experiments are headed: intended for behavioral engineering as well as value distribution, such tokens interface with the external world through wildly fluctuating markets.

Exhibit B: Creating ‘transactional communities’

Beyond the internal workings of decentralised networks, media scholar Lana Swartz describes emerging economic communities as ‘transactional communities’. Drawing on the idea of nations as ‘imagined communities’ she traces how a plethora of new digital payment systems symbolically and structurally are forming identities and belonging.

Payment apps increasingly resemble social networks. While different payment cards have for some time signified belonging to a certain social class and granting special privileges. The many different money mediums, in this sense, are sifting people into different social strata, where the rules of economic engagement are not always equal.

This is not the first time that money has taken multiple forms and functions. Quoting historian David Henkins, Swartz notes that in the context of the US, before a national state currency was enforced, these many monies were “part of the mystery of the city that could only be decoded by connoisseurs”.

This description would be apt for the cryptocurrency worlds of today, where instead of connoisseurs there are influencers, corralling the bright-eyed public through the realms of scammers and entrepreneurs, hackers and engineers. And instead of the city, there are networks, apps, platforms and bots.

.png")

Swartz also makes the point that money was an important part of building and consolidating nations. As a medium, its circulation, imagery and symbolism distributed a national imagination across territories, while its economic use tied people together despite the language differences in the US at that time. And indeed, global communities of affiliation are being formed around various crypto projects.

Exhibit C: Many moneys, much risk?

Swartz describes national currencies as one of the big 19th-century public infrastructure efforts, like the postal service and railroad. This is an informative way of thinking about not only national currencies, but as Brett Scott argues, specifically cash: as a public utility. Cash is a famously ‘fungible’ form of payment. A pound coin in the hands of a millionaire will be the same pound coin in the hands of a beggar. In fact, the early dreams of crypto was to ‘disintermediate’ digital payments from banks and governments to create cash in digital form, controlled directly by people.

Crypto claims to empower individuals, giving them more direct control.... but, in practice, often shifts risk onto them

While such aims of disintermediation might have been fine and good, at some point it becomes necessary to look soberly at what has happened since. And what's happened is an explosion of new intermediaries and unknown systemic risks.

The crypto world is becoming increasingly complex, now with several layers of tokens and market designs, facilitated by supposed stablecoins, in turn plugged into other payment platforms and commercial bank accounts and, in the end, denoted in the value of various national currencies – which continue to be the real tether to actual economies.

Much like in the 19th century, these many new monies might herald a new historical wave of re-consolidation in some form. In fact, states and central banks are beginning to show muscle and reassert control from crypto as well as the private banking industry and technology companies.

Shifting allegiances

All in all, the stakes are high, not least on the question of unprecedented economic surveillance, algorithmic control and who is really most at risk in these shifting conditions.

Crypto claims to empower individuals, giving them more direct economic control, and tends to emphasise privacy, but, in practice, all too often shifts risk onto individuals. Central banks are concerned with economic stability and managing systemic risk, but have very little incentive to protect people’s privacy. Private banks and big tech currently dominate payments, the latter having become a global oligopoly. Meanwhile, central bank digital currencies could very well bypass their growing power, challenging tech and banking monopolies by dealing directly with emerging FinTech and crypto industries.

It is indeed unclear which actor really has the public interest most at heart. For those of us concerned with democratic rather than oligarchic control over the economy and privacy rights, alliances might have to be struck with willing governments, technology companies and crypto platforms on an ad-hoc basis.

openDemocracy is also experimenting with new value sharing options through our CommentX feature supported by Grant For The Web. The best comments under this article will be highlighted by the author/editor and can receive a share of micropayments made to the article by Coil users. We invite your comments.